After a hailstorm rolls through Harris County, your insurance company sends someone to assess your roof. That person is an adjuster. But not all adjusters are on your side. Before you let the process play out on its own, Houston homeowners should understand exactly who is in the room and whose interests they represent.

The choice between relying on an insurance adjuster and hiring a public adjuster can be the difference between a fair settlement and thousands of dollars left unclaimed. If you are still early in the process, our storm damage insurance claims guide covers the full process from inspection to payout. Here is what you need to know about who represents you along the way.

Quick answer: An insurance adjuster is employed by your insurance carrier and evaluates your claim based on the company’s financial interests. A public adjuster is an independent professional who works solely for you and advocates to maximize your settlement. For large or complex roof damage claims in Houston, Texas, the Texas Department of Insurance reports that homeowners who hired professional representation received settlements three to four times higher than those who did not. Public adjusters charge up to 10% of the claim total for this service.

Schedule your free roof damage inspection with Big Easy Roof Claims before your adjuster visit and know exactly what your property is worth.

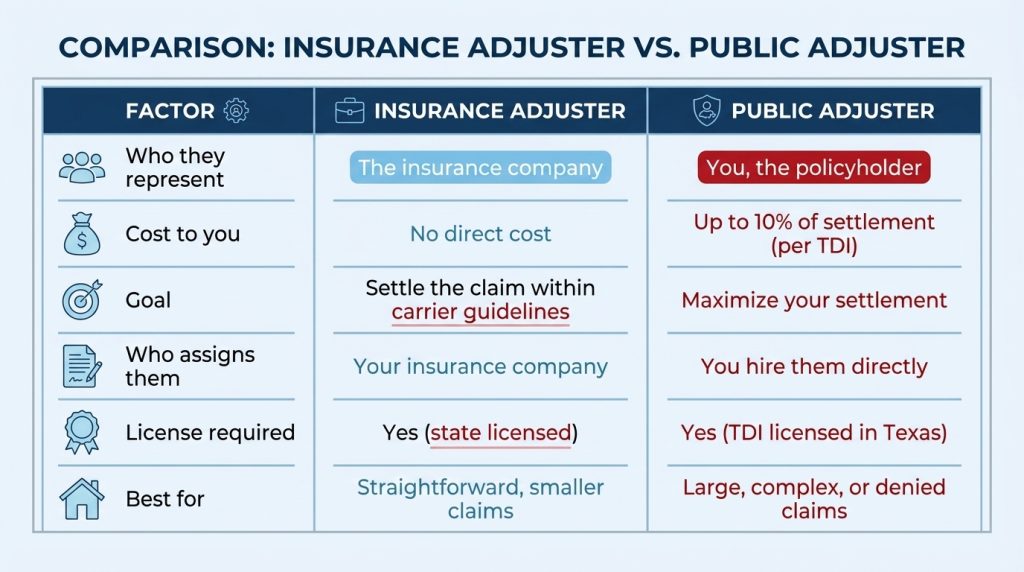

An insurance adjuster, sometimes called a company adjuster or staff adjuster, is a licensed professional employed by or contracted with your insurance carrier. Their job is to inspect your property, document the damage, and estimate the cost of repairs. That estimate becomes the basis for your settlement offer.

Insurance adjusters are not inherently dishonest, and many are genuinely knowledgeable about construction and storm damage. However, they work for the insurance company. Their assessments are made within the carrier’s guidelines, and items that fall outside standard documentation practices may be excluded from your claim, not because they are not covered, but because they were not identified.

In a city like Houston, where hail and wind events are frequent and damage patterns are complex, this distinction matters. Hidden damage, code upgrades required by Harris County, and interior water intrusion from roof penetration are the types of items a company adjuster may miss or undervalue.

A public adjuster is a state-licensed claims professional who represents policyholders, not insurance companies. They are hired directly by the homeowner to inspect the property, document all damage, interpret the insurance policy, and negotiate the settlement on the homeowner’s behalf.

In Texas, public adjusters must be licensed by the Texas Department of Insurance (TDI). You can verify any public adjuster’s license on the TDI website before signing a contract. The Texas Association of Public Insurance Adjusters (TAPIA) also maintains a directory of licensed members operating in the Houston area.

Public adjusters are paid on a contingency basis. They collect a percentage of what your insurance company pays out, which means they only earn more when you earn more.

The Texas Department of Insurance caps public adjuster fees at 10% of the total insurance settlement for standard claims. For claims involving a gubernatorially declared disaster, the cap is 10% for the first year after the declaration. These caps apply to signed contracts with licensed Texas public adjusters.

Most public adjusters work on a pure contingency basis, meaning no upfront fees. You pay only when your insurance company pays out. This structure aligns the adjuster’s incentive directly with your outcome.

Before signing any contract, verify the adjuster’s license on the TDI website and confirm the fee percentage in writing. The TDI also advises homeowners to read the entire contract before signing, including cancellation terms.

This is a critical question for Houston homeowners, and the answer is no. Texas law prohibits roofing contractors from acting as public adjusters or negotiating insurance claims on your behalf unless they hold a separate TDI public adjuster license. This practice, sometimes called “claim steering,” has been the subject of consumer alerts from Texas regulators.

A roofing contractor can legitimately provide a repair estimate, complete the approved work, and coordinate with your adjuster on scope. What they cannot do is represent you in negotiations with your insurer, advise you on claim strategy as a paid service, or receive a fee tied to the size of your settlement.

At Big Easy Roof Claims, we operate within these boundaries. We provide thorough documented inspections using drone and thermal imaging technology, prepare detailed repair estimates for your adjuster, and coordinate directly with insurance adjusters on scope, supplements, and code requirements. We do not charge fees tied to your settlement, and we do not cross the line that Texas law draws between contractors and licensed public adjusters.

Call (832) 924-6251 or request your free roof assessment and find out exactly what your storm damage is worth before your insurance adjuster arrives.

Hiring a public adjuster makes the most sense in the following situations:

An insurance adjuster is employed by or contracted with your insurance company and evaluates your claim based on the carrier’s guidelines and financial interests. A public adjuster is an independent professional, licensed by the Texas Department of Insurance, who you hire directly to represent your interests and negotiate the highest possible settlement on your behalf. The key distinction is who each one works for.

It depends on the size and complexity of your claim. The Texas Department of Insurance has documented that homeowners with professional representation received settlements three to four times higher than unrepresented claimants on contested or complex claims. For minor, straightforward claims, the public adjuster’s fee (up to 10% of the settlement) may outweigh the benefit. A detailed contractor inspection before filing can help you assess whether professional advocacy is warranted.

The Texas Department of Insurance caps public adjuster fees at 10% of the total insurance payout for most claims. Most work on a contingency basis with no upfront cost. You pay only when your insurance company pays. Always verify the fee percentage in your written contract before signing, and confirm the adjuster holds a current TDI license.

No. Texas law prohibits roofing contractors from acting as public adjusters or negotiating insurance claims unless they hold a separate TDI public adjuster license. A contractor can provide a repair estimate and coordinate with your adjuster on scope of work, but cannot represent you in negotiations or charge fees tied to your settlement amount. Working with a contractor who understands this boundary protects you legally and financially.

A public adjuster inspects your property, documents all covered damage, reads your policy to identify applicable coverage, prepares a detailed damage estimate, and negotiates with your insurance company on your behalf throughout the entire claims process. For roof damage specifically, they look for items that insurance adjusters commonly undervalue or miss, including hidden hail impact, code-required upgrades, and water intrusion damage.

Yes. You can hire a public adjuster at any point during the claims process, including after a settlement offer has been made or after a denial. Texas law gives policyholders the right to dispute claim decisions and reopen files with new documentation. Bringing in a public adjuster after an initial low offer or denial is one of the most common scenarios in which their involvement produces a significant difference in the final settlement.

If your Houston roof claim was denied or settled for less than the cost of repairs, contact us, as we provide a free damage assessment and detailed inspection report you can use to support a supplemental claim or dispute process.